By Diosh — Founder, AHAeCommerce | eCommerce decision intelligence for $50K–$5M GMV operators

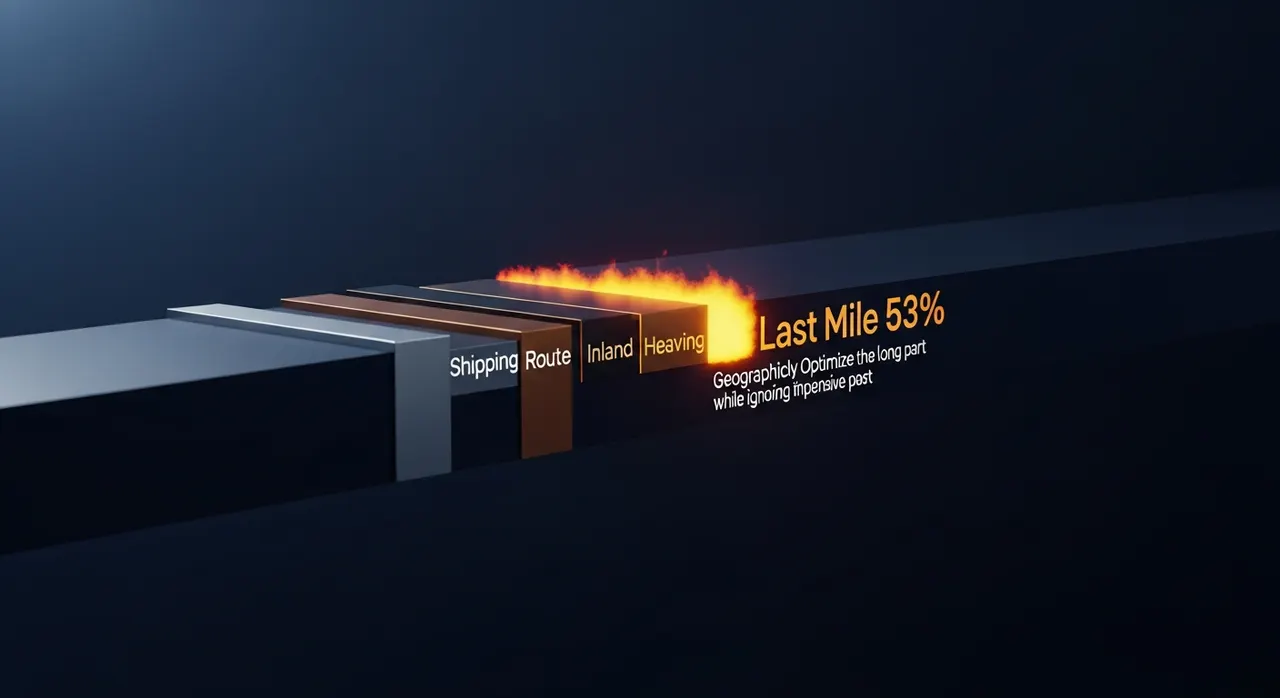

The last-mile leg of a shipment — the carrier's local depot to the customer's doorstep — represents 53% of total shipping cost in US eCommerce, per Capgemini's 2023 Last Mile Delivery Report. It is also the leg with the most operator leverage. Outbound zone, dimensional weight pricing, accessorial surcharges, residential delivery fees, and the difference between published rates and the rate the merchant actually pays compound into a cost structure most sub-$5M operators never audit at the line-item level. A typical $1.5M GMV operator running 18,000 packages/year through a single carrier at default rates pays $108K–$162K in shipping. The audit-based optimization — zone analysis, DIM weight challenge, accessorial reduction, multi-carrier routing — typically saves 12–22% of that, or $13K–$36K per year, with no operational change visible to the customer. Operators who have selected a 3PL with distributed fulfillment nodes gain an additional zone-optimization lever that single-warehouse operators don't have access to.

The reason most operators don't audit is that shipping invoices are presented as a single line item per package, not decomposed. The fee structure is opaque by design. Decomposing the structure is a one-time exercise that produces recurring savings.

What Last-Mile Cost Is Composed Of

The carrier rate the merchant pays is not the rate on the public rate card. The actual cost is built from six components, with each one negotiable or optimizable independently.

Component 1: Base Rate

The published rate per weight × zone, before any modifiers. UPS, FedEx, and USPS all publish annual rate cards with year-over-year increases of 5.9% (UPS 2024), 5.9% (FedEx 2024), and 5.5% (USPS 2024). The base rate alone goes up roughly 6% per year regardless of operator behavior.

Component 2: Zone

The geographic distance bracket from origin to destination. Zone 2 (within 150 miles) is the cheapest; Zone 8 (1,801+ miles) is the most expensive. The rate differential between Zone 2 and Zone 8 for a 2 lb package is typically 2.4–2.9x. An operator shipping from a single warehouse in the Midwest with customers spread across all zones pays meaningfully different effective rates depending on where the warehouse is located relative to the customer base.

Component 3: Dimensional Weight (DIM Weight)

Carriers charge by the greater of actual weight or "dimensional weight" — a calculated weight based on the package's volume. The DIM divisor is typically 139 for domestic ground (UPS/FedEx) and 166 for USPS. A package measuring 12 × 10 × 8 inches has a dimensional weight of (12 × 10 × 8) / 139 = 6.9 lb, regardless of actual weight. If the actual contents weigh 1.4 lb, the merchant is billed for 7 lb.

The DIM weight penalty is the largest invisible cost in eCommerce shipping. For brands shipping in oversized boxes — common for apparel because of warehouse picking efficiency — the DIM weight penalty often doubles the effective shipping cost. A pack-out audit reducing average box volume by 15% commonly saves 8–14% of total shipping spend.

Component 4: Residential Delivery Surcharge

Each carrier charges a flat surcharge for residential delivery — currently $5.85 (UPS Ground 2024), $5.65 (FedEx Home Delivery 2024), and $0 (USPS, structurally exempt). For an operator shipping primarily B2C with 95%+ residential addresses, this is a $5.65–$5.85 surcharge on every package, applied universally and rarely scrutinized.

Component 5: Accessorial Fees

The opaque category. Carriers apply additional charges for:

- Address correction: $20–$22 per occurrence (when the customer-entered address requires the carrier to correct it)

- Delivery area surcharge (DAS): $3.95–$5.85 for "extended" zip codes (rural and some suburban), with separate surcharges for "remote" zip codes

- Saturday delivery, signature required, hazmat, additional handling: each $4–$22 per package

- Fuel surcharge: 17–22% of total bill, varying weekly with fuel index

- Peak season surcharge: $1.50–$8.00 per package during November-December

For a typical $1.5M GMV operator, accessorial fees compound to 18–28% of total carrier spend. They are presented in invoice as small line items but aggregate meaningfully.

Component 6: Negotiated Discount

The published rate × (1 - negotiated discount %). Most operators with $50K+/year in carrier spend qualify for negotiated rates. Discount levels:

- $50K–$200K/year: 15–35% off published

- $200K–$500K/year: 30–55% off published

- $500K–$2M/year: 50–70% off published

- $2M+/year: 65–80% off published

The discount applies to base rate, sometimes to surcharges, rarely to all line items. Read the contract carefully — some carriers exclude DIM weight or accessorials from discount.

The Audit: What Most Operators Don't Know

Three numbers reveal the optimization opportunity. Most operators cannot answer these without pulling the data.

Number 1: Zone Distribution of Outbound Shipments

For a typical operator with one warehouse, zone distribution is heavily weighted by the warehouse location relative to customer geography. The audit:

Pull last 90 days of shipments from the 3PL or shipping platform. Group by zone (1-8). The shape of the distribution determines the optimization options.

If zones 5-8 represent more than 35% of volume: a second warehouse or zone-skipping strategy becomes economic. If zones 2-4 represent more than 70% of volume: the warehouse location is well-aligned with customer base; no multi-node investment justified.

Per ShipStation's 2024 customer benchmark data, the median single-warehouse operator ships 41% to zones 5+ — a meaningful share of high-cost shipments that could be reduced through warehouse strategy.

Number 2: DIM Weight Penalty (Average Billed Weight vs. Actual Weight)

For each package, billed weight is the greater of actual or dimensional weight. The audit calculates:

DIM penalty % = (Average billed weight - Average actual weight) / Average actual weight

A 0% DIM penalty means packages are dense enough that actual weight always wins. A 40%+ DIM penalty means packages are oversized — every package is paying for ~40% more weight than it contains.

For most apparel and home goods operators, DIM penalty runs 25–60%. Reducing it requires: smaller box inventory, packout standards (e.g., 95% box fill), or right-size packaging tools at the warehouse.

Number 3: Accessorial Fee Composition

Pull the carrier invoice (not the shipping platform's order-level cost — the actual carrier invoice with all line items). Categorize each accessorial:

- Address correction count: high count = address validation gap on checkout

- DAS / remote area count: high count = customer geography includes rural; pricing strategy needed

- Fuel surcharge total: typically 18–22% of bill; not directly negotiable but visible

- Peak season surcharge: only Q4; budget separately

Address correction fees are the most reducible. A simple Shopify/checkout app (Loqate, ShipperHQ address validation) catches 70–90% of address errors before label print, saving $20–$22 per caught error.

The Worked Cost Audit: $1.5M GMV Operator

Operator profile: apparel, 18,000 packages/year, single warehouse in Chicago, carrier mix 70% UPS Ground / 25% USPS Priority / 5% UPS 2nd Day Air, currently at 35% UPS negotiated discount.

Pre-Audit State

| Component | Annual Cost (USD) | % of total | |---|---|---| | UPS base rate × zone × discount | $58,400 | 47% | | USPS Priority Mail | $24,300 | 19% | | UPS 2nd Day | $9,600 | 8% | | DIM weight penalty (~38% on average) | $14,200 | 11% | | Residential surcharge ($5.85 × 12,600 packages) | $7,371 | 6% | | Address correction ($21 × 320 occurrences) | $6,720 | 5% | | DAS / remote surcharge | $3,800 | 3% | | Fuel surcharge | — | included above | | Peak season surcharge | $1,650 | 1% | | Total | $126,041 | 100% |

Optimization Pass

Zone analysis: 38% of shipments to zones 5-8. A west-coast 3PL secondary node would reduce ~half of those to zone 2-3. Cost of node: $15K setup + $0.45/order incremental fulfillment cost. Annual savings: ~$8,400 in shipping. Payback period: 4 months. Implement.

DIM weight: Audit reveals 60% of packages ship in size "Medium" boxes when "Small" would suffice. Box re-sizing program: $1,800 in new box inventory, 1 hour/week of warehouse retraining for 3 weeks. Annual savings: ~$5,500. Implement.

Address correction: Loqate address validation app: $99/month = $1,188/year. Reduces address corrections by 80%. Annual savings: $5,376 - $1,188 = $4,188 net. Implement.

Negotiation: At $126K/year, the operator qualifies for 40-45% UPS discount; current is 35%. Renegotiation conversation. Estimated savings: $3,200/year. Implement.

Multi-carrier routing: Test FedEx alongside UPS for zone 5-8 shipments where FedEx Ground rates are sometimes 8-15% cheaper. Annual savings: ~$2,400. Implement.

Post-Audit State

| Optimization | Annual Savings | |---|---| | Zone strategy (secondary node) | $8,400 | | DIM weight (box right-sizing) | $5,500 | | Address correction (validation app) | $4,188 | | Carrier renegotiation | $3,200 | | Multi-carrier routing | $2,400 | | Total annual savings | $23,688 |

The audit produces 18.8% reduction in shipping cost. Total operator time investment: roughly 40 hours over 6 weeks. Implementation cost: ~$17K (mostly the secondary node setup), recovered in under 6 months.

The Carrier Negotiation Reality

Most operators believe carrier negotiation is for enterprise volumes. It is not — it is for any operator above $50K/year in carrier spend who has not renegotiated in 18+ months.

The negotiation levers:

Lever 1: Volume Commitment

Promise a specific monthly minimum in exchange for a higher discount. Works when the operator has growth visibility and can commit credibly.

Lever 2: Mix Commitment

"We'll route 80% of our shipments through you" instead of multi-carrier. Carriers prefer dominant-share relationships.

Lever 3: Multi-Carrier Threat

Genuine quotes from competitive carriers (FedEx if currently UPS, vice versa) used as leverage. Most carriers will match or beat a credible competitive bid, but only if the merchant has actually engaged the alternative.

Lever 4: Anniversary Renegotiation

Request a rate review at every contract anniversary. Carriers do not proactively volunteer better rates as volume grows; the operator must ask.

What Operators Should Not Do

Negotiate against published rates only. The discount % means little if applied against a different base. Carriers compete on different surcharge structures — a 50% discount with zero accessorial discount is worse than a 40% discount with 15% accessorial discount for most operators.

Always model effective per-package cost across the typical mix, not the headline discount %.

The Verdict

Last-mile is the largest single-line eCommerce cost outside acquisition and product cost. It is also the least audited at a structural level. The operators who run the audit — zone, DIM, accessorial, negotiation — typically recover 12–22% of total shipping spend in the first quarter, with most of the savings recurring annually. Operators adding international destinations should model last-mile separately per country, as the cost structure diverges sharply from domestic economics.

The audit is not glamorous. It requires pulling carrier invoices, categorizing line items, calculating zone and DIM distributions, and having a competent negotiation conversation. The work is unsexy. The leverage is real. For most sub-$5M operators, last-mile audit is the highest-ROI 40 hours of operator time available, full stop.

This Week

Pull last 90 days of carrier invoices (the actual carrier invoice, not the shipping platform's summary). Categorize: base rate vs. surcharges vs. accessorials vs. fuel. Identify the largest accessorial line item — for most operators, it will be DIM weight or address correction. Address that one. The single highest-leverage line item, addressed in isolation, typically pays for the audit time multiple times over within the first quarter.